First Time Home Buyer Incentive Bc Things To Know Before You Get This

Table of ContentsAbout First Time Home Buyer Incentive BcThe Main Principles Of First Time Home Buyer Incentive Bc The 8-Minute Rule for First Time Home Buyer Incentive Bc9 Simple Techniques For First Time Home Buyer Incentive Bc

00:00:38 which is why the incentive is registered as a bank loan on the home. Visual: The video reduces to a split-screen shot. On the left 2 thirds, a couple as well as their little one are resting close together at a table having fun with a game and also, on the ideal 3rd, a vertical yellow band appears with the following text created in purple: "motivation is signed up as a bank loan on the residential property" 00:00:43 There are, however, Visual: The text in the yellow band on the ideal 3rd on the display is changed with the following: "no routine principal settlements no passion maximum term of 25 years" 00:00:44 no routine major settlements, 00:00:45 it births no interest, 00:00:47 and it has an optimal term of 25 years.ca" 00:01:40 To learn exactly how to use, 00:01:41 check out the last video clip in this four-part series. Aesthetic: Versus the yellow history, the following text shows up: "Have a look at the last video clip in the collection" Listed below it, there is a white sketch of a residence with shrubs and also a tree - first time home buyer incentive bc.

The shot after that reduces to a full-screen white history. Versus it are the yellow, purple as well as grey National Real estate Strategy logo design, left wing, and the Canada Wordmark, on the right.

First Time Home Buyer Incentive Bc for Beginners

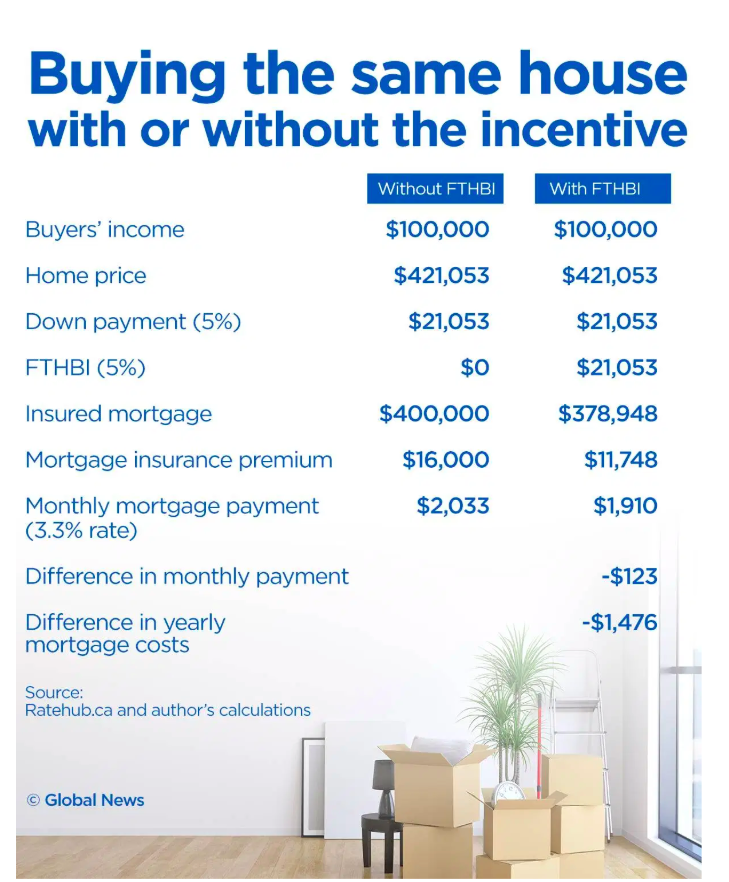

When genuine estate costs ascend into the air, down repayments are dragged along for the ride producing a problem for novice residence customers (first time home buyer incentive bc). Potential purchasers may stretch a dollar, conserve and also compromise their means to a minimum down settlement only to figure out that the staying mortgage quantity greater than loan providers want to accept.

FTHBI candidates must: Be a Canadian citizen, irreversible resident or lawfully authorized to operate in Canada. Be a novice home customer, indicating you have never owned a home. Homeowners who have undergone a separation or break down of a common-law collaboration are also qualified, as are those who have actually not lived in a home that they possessed (or that was had by their spouse or common-law companion) for the last four years.

Be pre-approved for a mortgage that is much more than 80% of the residential or commercial property's worth, as well as thus covered by home loan insurance. Compare Canada's top home mortgage loan providers as well as brokers side-by-side and figure out the very best mortgage rates that will fulfill your requirement Qualified residence purchasers can apply for the FTHBI once they have actually been pre-approved for a home loan by a home loan lending institution and located your house they wish to get.

5 times your earnings. Your total home earnings can't be higher than $120,000. Under the terms of the Incentive program, the mortgage can't be even more than 4 times your earnings.

How First Time Home Buyer Incentive Bc can Save You Time, Stress, and Money.

If you reside in Vancouver and also gain the house max of $150,000, one of the most you could obtain from a mortgage lending institution and also still be accepted for the FTHBI program is $675,000. If your house makes also a buck more than those earnings limits, or there are no residences offer for sale within the cost limits developed by the government, your application for a FTHBI lending will not be authorized.

Because you've become part of my latest blog post a common equity contract with the government, they essentially possess 5% or 10% of your residence. When that home obtains sold, with any luck for more than you initially paid, they're entitled to remove the very same percent of equity, however it's based upon the present market value as opposed to the initial acquisition.

Let's claim you discover a $500,000 condominium in Vancouver, and also you obtain a FTHBI finance of 5% of the acquisition cost, or $25,000. When you choose to market the home 10 years later on, it's worth $800,000. At the time of sale, you'll owe the FTHI program 5% of the price not the $25,000 you originally obtained, but $40,000 (first time home buyer incentive bc).

Paying back much more than what you borrow is bound to sound iffy to some individuals, but the program isn't planned to assist home proprietors maximize their earnings. It's regarding obtaining novice purchasers right into a home when there are couple of various other choices.

Things about First Time Home Buyer Incentive Bc

You can repay it at any time you such as, without marketing your house as well as scot-free. Your settlement will be based on 5% or 10% of the residence's value at the time, as established by a specialist appraiser Beginning a residence purchase with a bigger down payment means obtaining a smaller sized home mortgage, which must bring about less interest costs as well as smaller month-to-month settlements.

By reducing the expense of your mortgage, the FTHBI might get you into a home when nothing else program can. Certain, you could need to pay back see post greater than you obtained, but think of the equity the FTHBI loan could assist you build up in the meanwhile. If your building increases in value, you'll need to repay two times what you borrowed, but those tens of hundreds of dollars will be repaid out of numerous hundreds of bucks in revenue earnings you would not have gained without the FTHBI.

You can repay the finance completely at any kind of time prior to the 25-year home window closes, giving you an opportunity to leave the program before your residence has time to value at as well torrid a advice pace. The earnings and also residence assessment limitations may be as well reduced to aid many homes discover housing that satisfies their demands.